This fall we saw mostly continuation of trends from the summer best described as splitting of the investment world. The prospects of a Covid19 vaccine and US government spending triggered major shifts in currency and certain stocks continued to part ways with the herd.

Bonds and Interest Rates

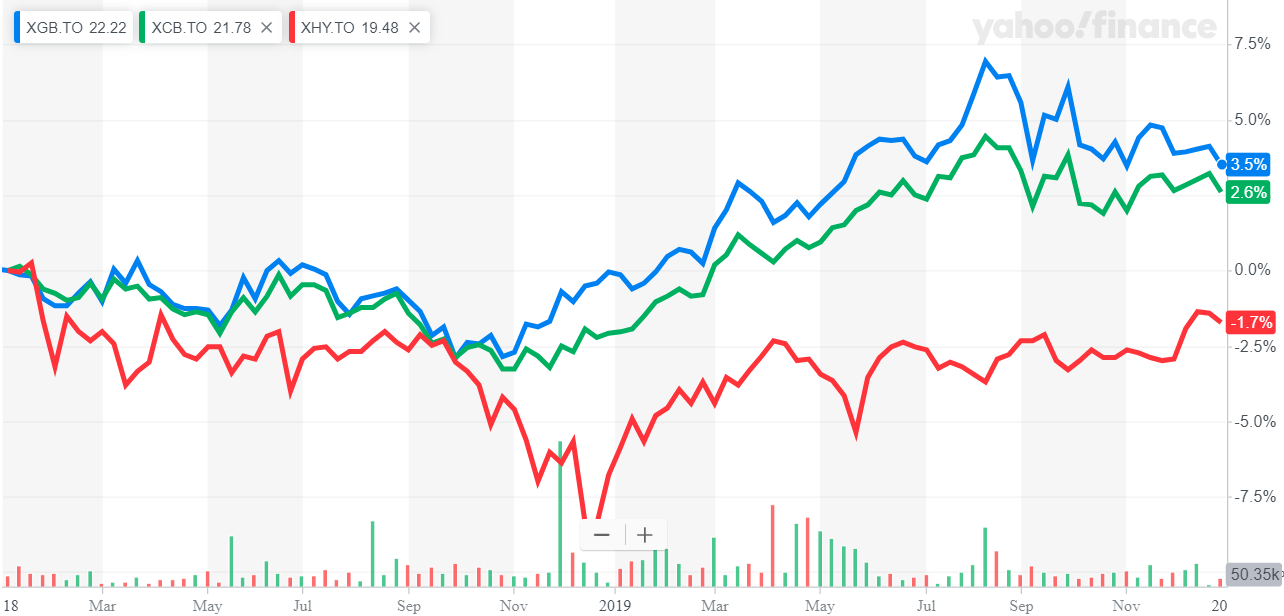

You can see from XGB charted below that government bonds peaked at the beginning of August and have gradually declined since then. This is in line with an investment world getting more comfortable with the state of the Covid19 world and drawing money away from safe haven investments toward more risky investments. Meanwhile, investment grade corporate bonds (XCB) dipped into the beginning of November and recovered after that while high yield bonds continued to rise through the quarter. This decline in government bonds and rise in high yield (i.e. higher risk) corporate bonds illustrates the shift from safer to more aggressive investing.

I would note that a lot of the survival of certain at-risk corporations has come from government subsidies, government buying corporate debt, bank loan deferrals, and various other tactics to prop them up. This means you shouldn’t exactly interpret the shift toward corporate investing as a sign these companies are once again in good stead. The reality is that many lower grade corporations are on life support.

Fig. 1: Bond ETFs: Governments (XGB), Corporates (XCB), High Yield (XHY) – 2 years

The transition from a Republican-led to Democratic-led US Senate (only fully clear after the two Georgia senate races concluded after the year-end) means there is increased US government appetite for spending to prop up the economy and so investors largely feel the government has got their back.

Late in the year we saw long-maturity government bonds fall dramatically, illustrated by TLT. This signals investor belief (due to government spending and also the vaccine roll-out) that the government will successfully navigate the economy to a recovery and with the huge inflationary effect of all that government spending, interest rates will rise in the long run.

Traditionally, when government bond prices fall (implying interest rates rise) it has presented a good opportunity to buy bonds and the like. Ultimately they change course and rise back up. Note however that since the peak of interest rates in 1981 we have experienced a 40-year decline in interest rates (which means bond prices rising). For bond investors, the wind has been at our back, so-to-speak. Now, with interest rates for long maturity government bonds barely above 1%, is that still a realistic expectation? It’s not so certain. As a result, when the stock market heats up, these days we are more likely to look for lower cyclical stocks, rather than shift to government bonds. That said, there is still a place (but smaller) for the stabilizing effect of government bonds in many portfolios.

Currencies

In general, government spending is inflationary and devalues a currency (at the rate of inflation). Typically, we associate this phenomenon with small emerging countries with poor fiscal discipline but in 2020 it became clear that the immense government spending to keep the US economy from totally falling apart, combined with the US Federal Reserve commitment to keep interest rates low even in the face of inflation above 2%, meant there was a partial exodus from US dollar holdings. From its high on 23 March, 2020, the US dollar fell 12.6% versus a basket of other currencies.

Fig. 2: US Dollar Index and Canadian Dollar versus the US Dollar – 2 years

A decline in the USD is usually associated with a “risk-on” investing stance. That unfolds because when investors are more at ease they sell US dollars and buy foreign currency to invest further abroad. On the other hand, when US investors get panicky, they sell their foreign investments and bring their money back to the US, pushing the US Dollar up. For us, as investors with part of our portfolio in US stocks, I have noted before that this currency impact means that when stock markets falter our decline is muted because the rising USD partially offsets the falling market. On the other hand, when the stock market is soaring, the typically sliding USD dampens our upside. Overall the impact smooths our portfolio but this fall has been one of those “dampening our upside” phases. It would sound nice to jump into and out of US investments according to the stage of this cycle but of course being able to execute on that time after time after time is in my mind naively optimistic. It’s better to think about long term strategic portfolio construction and put together US and Canadian exposure that helps us in the long run.

That being said, we do always think about where to put to work our incremental cash whenever we have cash sitting on the sidelines and a weak US Dollar does at times tilt the investing table in favour of buying US stocks. Now is likely such a currency-induced tilt.

Stock Markets

Usually when reviewing stock markets I use indices from around the world to convey how different parts of the global economy are doing. Broadly speaking the US stock market has outperformed other markets around the world but the question is why. It is not precisely the better US economy, it is more driven by the fact that the US stock market contains more high technology stocks than any other stock market in the world. Therefore, digging a bit below the surface we can see that the difference is really driven by techs stocks versus non-tech stocks. The top 52-week performers in the S&P500 index are dominated by the likes of Tesla, Etsy, Nvidia, Paypal (all high technology stocks). Meanwhile other parts of the market just inch along to varying degrees.

As was the case with the dot-com implosion of 2001, some of these high-flyers are trading at nose-bleed prices. For example, Tesla is trading at 204 times next year’s earnings. That means if Tesla were to start paying out investors all the company’s annual profits as dividends and were able to maintain that profit level it would take investors two centuries to break even! Maybe Tesla will do well and double its profitability. Then it would only take one century, not two to break even! For anybody who has been investing a while, this is reminiscent of Nortel. Take a look at the charts below. On the left is the market during the three-year period from 1999 to 2002. On the right is the three-year period starting in 2019. The red line is the QQQ, indicative of tech stocks. The blue line is the SPY, indicative of the broader market. The intense escalation of tech stocks is astounding, once again. The difference this time around is that tech stocks have infiltrated the SPY more, so this time tech stocks are driving the broader index up too, while the rest of the stock market just trudges along.

When looking at other fad investments, the likes of bitcoin illustrate that there is extreme bullishness (i.e. buyer beware) in various corners of the market. Government stimulus may push the market higher but things are looking pretty frothy right now.

With that in mind here is what we have been doing. We have found various businesses trading at modest prices and also some reasonably priced preferred shares. For the most part the businesses we have found are not part of the ra-ra trend. We have been buying positions in the likes of Unilever, Loblaws, and Hydro One, all what I would consider very stable businesses. We have also found preferred shares in utilities, grocers, and the like, yielding dividends in the 4-6% range.

Furthermore, with the economy so frothy and also with the chance of inflation triggering possible further US Dollar depreciation around the corner we have taken a step that I have not taken during my investment career: we have taken a position in Barrick, a gold stock. To a large extent the price of Barrick moves with the price of gold and the price of gold moves with inflation fears. Essentially this position is a hedge against runaway inflation, given all the government spending. I am hopeful that it is not needed – that inflation is deftly managed by central bankers and our gold stocks do little while our other stocks do well. That said, it does provide protection. Barrick peaked this summer around $40/share before falling back. Depending on the account we bought some Barrick shares just below $34/share and more shares in the $29s. Lately it has been trading between $28½ and $31½. We will see how necessary the protective hedge was in the year ahead.

Fig. 3: Tech stocks in red, broader market in blue – 1999-2002 on the left, 2019-2022 on the right

In terms of selling, we have been reducing long-held positions in some of our high-flyers such as Maxar (the latest incarnation of the old McDonald Dettwiler/Spar Aerospace/ Loral Systems). Another example of a good company trimmed back is CME Group (the Chicago Mercantile Exchange), which runs financial exchanges. We still like the company but have to be prudent. At the same time there has been a bit of portfolio housecleaning. Western Union was sold. While the company is impressively well-entrenched around the world, in reality there are many different technologies such as cell phone money transfers, cross border bank cards, etc. that are all nipping at its heels. In the end WU might come out a winner in the international money transfer business but the way I see it, it won’t be easy. Parting with solid businesses is a hard thing to do but portfolio pruning is our job.

Respectfully submitted,

Paul Fettes, CFA, CFP

Chief Executive Officer,

Brintab Corp./Efficertain Corp.

Leave a Reply